Buying property through a self-managed super fund (SMSF) has become a familiar strategy for Australians wanting more direct control over their retirement savings, but it comes with a genuinely different set of rules to a standard investment property purchase — and getting the structure wrong can carry serious compliance consequences.

What an SMSF Property Purchase Actually Involves

An SMSF can purchase property as an investment for the fund, provided the purchase satisfies the “sole purpose test” — meaning the property must be held purely to provide retirement benefits to fund members, not for personal use or benefit along the way. This immediately rules out buying a holiday home or any property a fund member or their relatives intend to live in or use, with limited exceptions for certain business real property arrangements.

Borrowing Within an SMSF: Limited Recourse Borrowing Arrangements

If the SMSF doesn’t have enough cash to buy the property outright, it can borrow using a Limited Recourse Borrowing Arrangement (LRBA). Under an LRBA, the property is held in a separate trust until the loan is repaid, and critically, the lender’s recourse is limited to that specific property — it can’t claim against the fund’s other assets if something goes wrong. LRBA lending typically comes with stricter deposit and serviceability requirements than a standard investment loan, and not all lenders offer this product, so shopping this specifically with a broker experienced in SMSF lending matters.

Costs and Compliance Obligations

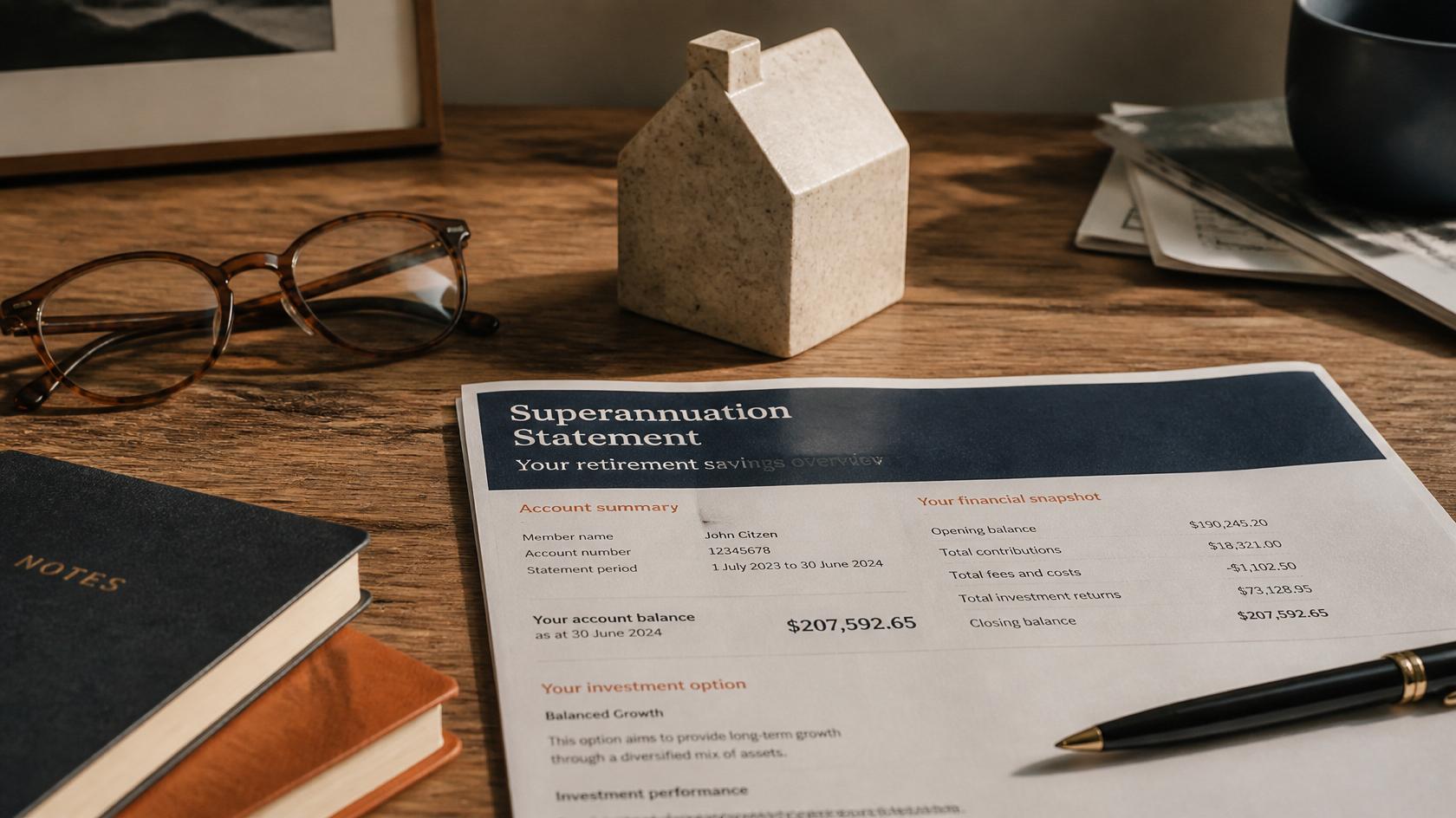

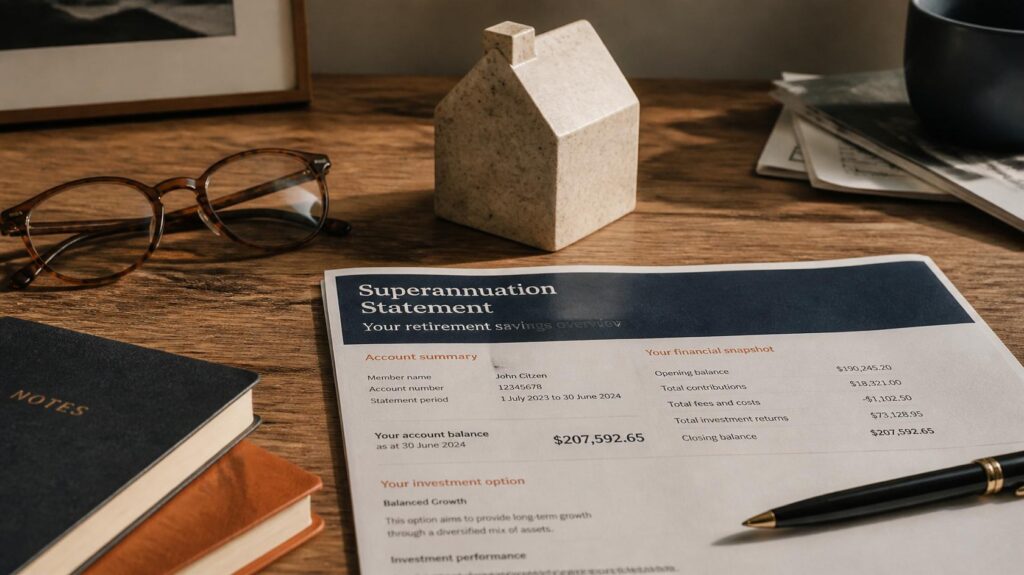

An SMSF property purchase involves setup costs beyond a standard purchase — establishing the bare trust structure, ongoing SMSF administration and audit fees, and specific legal documentation for the LRBA. The fund must also continue meeting its annual compliance obligations (audit, tax return, investment strategy review), and the property itself must be managed strictly in line with super regulations — for example, rental income must go back into the fund, not to members personally, and any renovations generally can’t be funded via further borrowing under the same LRBA in some circumstances, which is a common trap for first-time SMSF property investors.

Who This Strategy Tends to Suit

SMSF property investment tends to suit members with a reasonably substantial existing super balance (given the setup and ongoing costs involved relative to the investment size), a genuine long-term investment horizon, and a clear-eyed understanding that this is a retirement savings vehicle, not a flexible personal investment. It’s generally not well suited to buyers looking for short-term flexibility or who might need to access the property or the fund’s capital before retirement.

The Professional Advice You’ll Need

An SMSF property purchase genuinely requires a team, not a single adviser: a financial adviser to confirm the strategy suits your broader retirement position, a specialist SMSF lender or broker for the LRBA, and a solicitor experienced in SMSF trust structures to set up the bare trust correctly. Firms like Chamberlains work specifically in this kind of legal structuring, and engaging that expertise early — before you make an offer on a specific property — avoids the common mistake of finding a great property and then discovering the structure can’t be finalised in time.

If you’re weighing an SMSF purchase against a standard investment loan structure, our guide on investment property vs owner-occupier loans is a useful comparison point for the standard alternative.

Frequently Asked Questions

Can my SMSF buy a property from a fund member or their relative?

Generally no for residential property — acquiring an asset from a related party is heavily restricted under superannuation law, with limited exceptions for certain business real property; always confirm with a specialist SMSF adviser before considering this.

Can I live in a property my SMSF owns once I retire?

Generally no, while the property remains held within the SMSF structure — the sole purpose test continues to apply, and transferring the property out of the fund to yourself involves its own set of rules and potential tax consequences.

What happens if my SMSF can’t make loan repayments under an LRBA?

Because recourse is limited to the specific property under an LRBA, the lender’s claim is generally restricted to that asset rather than the fund’s other holdings — but this doesn’t remove the fund’s obligation to manage the loan responsibly, and default still carries serious consequences for the specific property and the fund’s compliance status.